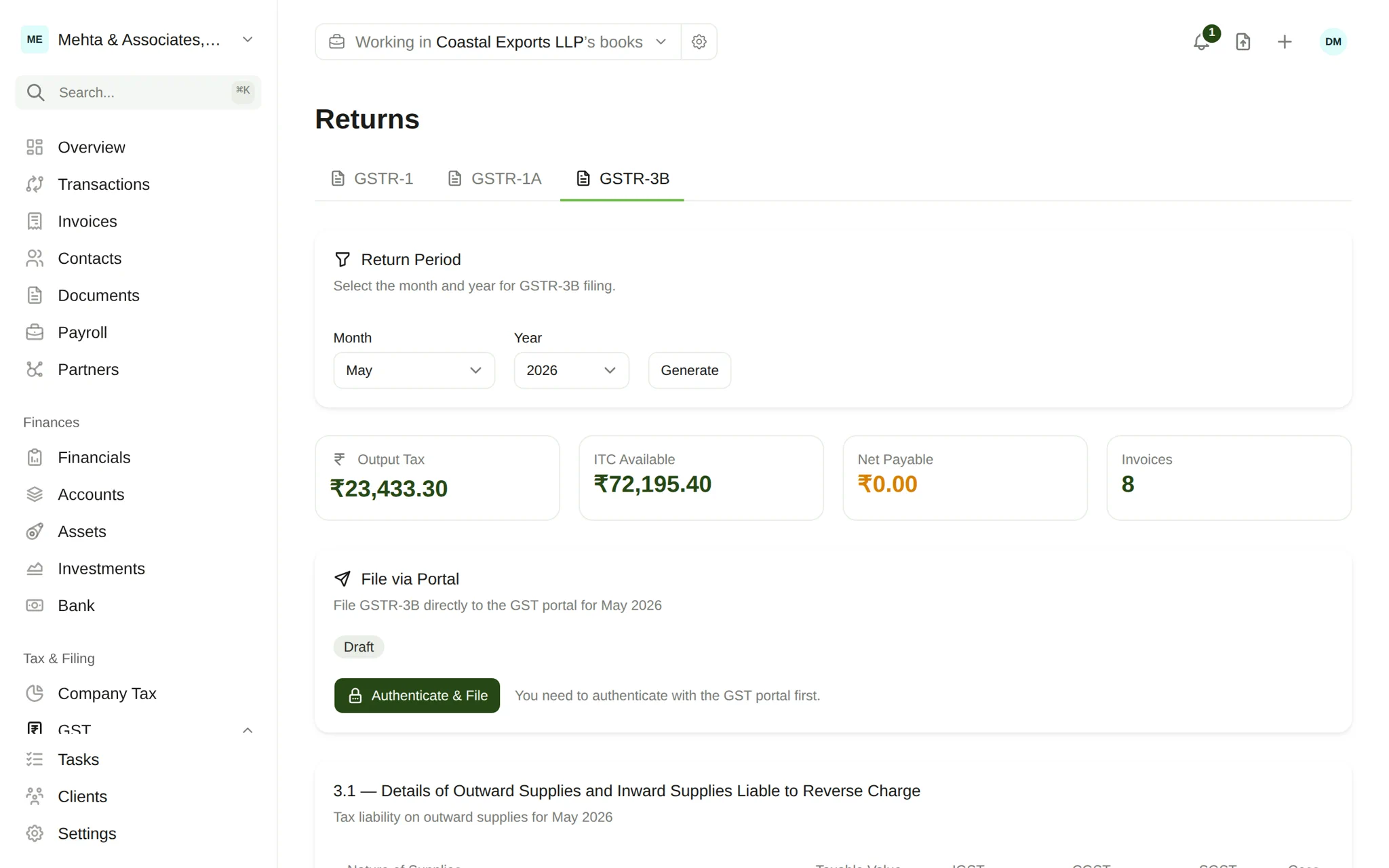

GST filing is rarely hard because the law is hard. It is hard because it is repetitive, deadline-bound, and spread across dozens of clients who all send their data late and in different shapes. A practice that files well is not the one that knows the most obscure rule — it is the one that runs the same disciplined workflow for every client, every cycle, without dropping a step.

This is the checklist we see high-functioning CA practices converge on. Treat it as a template you adapt to your own engagement letters and software, not as statutory advice — always verify rates, slabs, and due dates against the current law before you file.

1. Collect data on a fixed cadence

The single biggest cause of a missed GST deadline is data that arrives the night before. Move data collection off the filing week entirely.

- Set a recurring ask. Every client should know exactly what you need and when — sales registers, purchase invoices, expense bills, bank statements, and any credit/debit notes for the period.

- Standardise the format. A consistent template (or a direct integration that pulls the data for you) removes the back-and-forth of chasing missing columns.

- Track receipt, not just the request. A request that was sent is not data that arrived. Keep a per-client status so you can see, at a glance, who is complete and who is blocking.

A practice that closes data collection a week before the due date almost never files late. A practice that starts collecting on the due date almost always does.

If chasing clients for documents is eating your filing week, that is exactly the problem our data-in integrations are built to remove.

2. Reconcile before you compute

Reconciliation is where filings are won or lost. Do it before you touch the return, not after.

- Match purchases to the auto-populated inward supplies. Flag invoices that appear in your client's books but not in the portal data, and vice versa.

- Resolve mismatches with the supplier, not the return. A missing invoice is a vendor problem to chase, not a number to quietly adjust.

- Check the eligibility of input tax credit line by line — blocked credits, personal-use portions, and anything outside the period.

- Reconcile output liability against the sales register and any e-invoices or e-way bills generated for the period.

Only once the books and the portal agree should you move on. Computing a return on un-reconciled data just means you file twice.

3. Review, then file

The computation is the easy part once the data is clean. The review is what protects the client — and the practice.

- Run a second pair of eyes. A maker-checker step, even a light one, catches the transposed figure and the wrong period before it becomes an amendment.

- Sanity-check the headline numbers against the prior period and the same period last year. A 10x swing is a question, not a number.

- Confirm the cash/credit ledger has enough balance to cover the liability before the filing window, so a payment delay never becomes a late return.

- File, capture the acknowledgement, and store it against the engagement — the proof of filing is part of the record, not a loose email.

4. Close the loop

A filed return is not a finished job until the client and your own records reflect it.

- Send the client a clear confirmation — what was filed, the liability, and what they owe and by when.

- Log the next due date the moment you close the current one, so the next cycle starts from a calendar, not from memory.

- Note any open items (a chased invoice, a disputed credit) so they surface in the next cycle instead of being rediscovered.

FAQ

How early should I start the GST filing workflow for a client?

As early as the data allows. The work that actually takes time — collection and reconciliation — has nothing to do with the due date. Decouple it: collect on a fixed monthly cadence, reconcile as soon as data is complete, and leave only review and submission for the filing window.

What is the most common avoidable filing error?

Filing on un-reconciled data. When the books and the portal data disagree and the return is filed anyway, the result is almost always an amendment, a notice, or a lost input credit. Reconciliation before computation prevents nearly all of it.

Can this checklist replace professional judgement on rates and thresholds?

No. This is a workflow, not a rulebook. Statutory slabs, thresholds, and due dates change, so confirm every rate and date against the current law for the relevant period before you file.

Running this loop by hand across a portfolio is exactly the kind of work WeKeep is built to absorb — collection, reconciliation status, and review in one cockpit instead of a spreadsheet and a dozen inboxes. See how it is priced for practices, then join the waitlist to try it on your own clients.